Best Way to Invest and Save for a House

What is the best fashion to save money for a house? This is an interesting question and the one-time communication might require a new perspective given the reality of the current housing market. Home prices have changed dramatically over the last few years and this is impacting how people are making decisions around home buying.

Over the final few years we've seen the boilerplate dwelling house price increase faster than our ability to salvage for a downwards payment. This tin brand it difficult to save money for a house and this tin push home ownership to after stages in life.

This trend in home ownership has been happening for decades, with home buying shifting later and later. This may be due to a number of factors but there is a definite tendency towards purchasing a home afterwards in life.

In 1981 approximately 55.v% of those who were over historic period xxx lived in their own home.

In 2022 approximately l.2% of those who were over historic period 30 lived in their own abode.

With the continued increase in home prices since 2022 information technology's reasonable to presume that dwelling house buying will continue to shift into the xxx+ age group.

So if purchasing a home is happening later in life, does that modify the way nosotros save coin for a business firm? Does that modify the way we build up our down payment?

Conventional fiscal advice would suggest that whatsoever savings required in the next i-5 years should be kept in something safe, like a GIC or a high-interest savings account. Historically this meant that savings for a downwardly payment would get into i of these safe investment vehicles.

Just what if someone is starting their career in their early 20'southward and isn't planning to buy a home until their early on xxx's, late-30's or perchance even their 40's? Should they all the same be saving for a downward payment in a safe investment like a GIC?

Maybe, or perchance non. In this post we'll explore a different way to save money for a house. A fashion that is perhaps more than reflective of purchasing a domicile later in life.

How Much Practice You Need For A Downwardly Payment?

Currently the minimum amount yous need for a downwards payment is v% of the purchase cost. This is the absolute minimum that you need for a down payment, however many people aim for a college amount.

Buying a dwelling with a 5% downwards payment ways that yous're triggering mortgage insurance fees. These range depending on the % down payment only generally subtract as the % down payment gets larger. Mortgage insurance fees subtract every bit the downpayment crosses the 10%, fifteen% and 20% thresholds.

Abode purchases with over 20% downwards payment may not demand mortgage insurance at all (although it tin still happen where a lender requires mortgage insurance fifty-fifty with twenty%+ downwards)

This ways that having a 20% down payment has historically been the goal for many potential homeowners.

But when home prices are increasing, peculiarly when they're increasing in a higher place the rate of inflation, reaching a twenty% down payment can be more difficult. It requires a higher savings rate and there is ever the risk of getting "priced out of the market".

Timelines Are Of import

Timelines are important when it comes to fiscal goals, and purchase a home is no different. For shorter time frames we want to decrease the financial take a chance. Nosotros desire to ensure we take the coin available when nosotros need it. This usually means using a safe investment vehicle similar a GIC or a high-interest savings account. Both have a lower rate of return, typically in line with inflation or perhaps a chip more than.

For longer time frames we want to allow our savings to grow and compound. This makes it much easier to accomplish our goal. This usually means investing in a portfolio of stocks and bonds. Over the long-term this can provide a rate of return higher up inflation. With a higher rate of return in that location is more risk, in that location might be large swings in the short-term, but over the long-term we hope to run into a higher return.

Traditionally when saving for a business firm we would consider that a short time frame. We're typically saving upward a down payment over 1-5 years before buying a house and for that reason we would typically recommend a safe investment vehicle to concur that down payment.

But if a abode purchase isn't on the firsthand horizon perhaps we should exist taking a bit more risk with our down payment, or at least a portion of it. What if nosotros split our down payment goal into two.

One downwards payment goal could exist for five% of our down payment. This is the minimum. This amount should be invested in a safe investment vehicle.

The second downwardly payment goal couple be for the remaining v% to 15% of our downward payment. This is the "overnice to have" portion of our downward payment and could exist invested in a low-cost portfolio and allowed to abound more quickly over time.

Let's explore what this looks like with actual investment returns from the past… but first, where is the best identify to hold your downward payment…

TFSAs And Saving Upwards A Downward Payment

TFSAs are a great way to save up for a downwards payment. The TFSA allows contributions to be invested and grow tax gratis. Withdrawals tin can be fabricated at whatsoever fourth dimension and that contribution room comes back the following January.

TFSAs are a great mode to salvage upwardly a downward payment.

TFSAs are also interesting because they can be used as an investment account also. It'southward possible to accept two TFSAs, one for safe investments like GICs or a loftier-interest savings business relationship, and a second for investing in a low-cost investment portfolio.

RRSPs And The Abode Buyers Program

RRSPs are some other option for saving up for a down payment just information technology becomes a bit more complicated. In full general RRSPs are a prefered investment vehicle when you have a high revenue enhancement rate now and expect a lower revenue enhancement rate in the hereafter. This isn't necessarily the case for individuals saving upwards for a down payment.

Using an RRSP instead of a TFSA may not exist the best selection, particularly if you lot await your earnings to increase apace in the future (which is a reasonable expectation for new grads in their starting time job).

RRSPs are highly-seasoned when buying a house for one reason, the Abode Buyers Programme. In that location are some qualification criteria around the Home Buyers Program but essentially it allows individuals to withdraw upwardly to $35,000 from their RRSP without triggering income revenue enhancement. This amount needs to be repaid to the RRSP over 15-years. For a couple this means a potential $70,000 in RRSP withdrawals that can exist used for a home buy.

Depending on your electric current tax charge per unit the RRSP Domicile Buyers Program could be a great choice. It can also be a skilful choice when yous've already maximized your TFSA.

Saving Up A Down Payment vs Saving And Investing Hybrid

Allow's look at two options for saving upwardly a down payment. One where we save the total twenty% down payment in a high-interest savings account earning 2.1% and a second where we save the minimum 5% downwards payment in a high-interest savings account just then invest the rest in a low-price investment portfolio.

We'll assume a couple (or ii individuals) who are each putting $500/month toward their down payment goal. They want to purchase a abode worth $600,000 in today'south dollars and ideally accept $120,000 for their downward payment.

Obviously with the investment choice we're taking on a lot of actress adventure. But we're going to presume nosotros have a 10-twelvemonth horizon earlier purchasing a house. But fifty-fifty with a 10-year time horizon we might meet our strategy fail in some periods of poor stock/bail returns.

Lastly, nosotros're going to look at everything in today's dollars, so we're going to remove inflation. We'll presume aggrandizement is 2.1%, substantially equal to the involvement rate on the high-interest savings account.

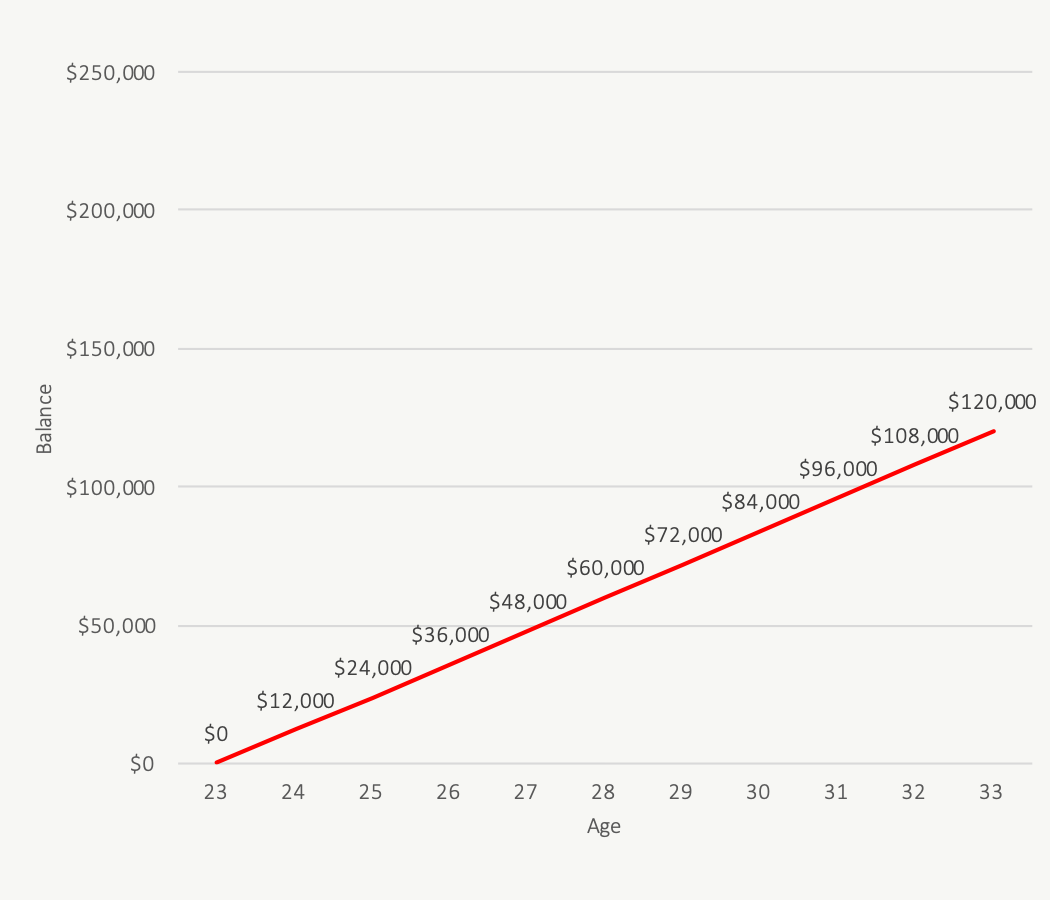

Saving Upward A Down Payment Over ten Years

Considering nosotros're looking at today'south dollars (real dollars) the balance in the high-interest savings account goes upward by the contributions each year. If we were to look at this in time to come dollars (nominal dollars) then we would see this balance increase with the involvement rate (which nosotros've causeless to be equal to inflation).

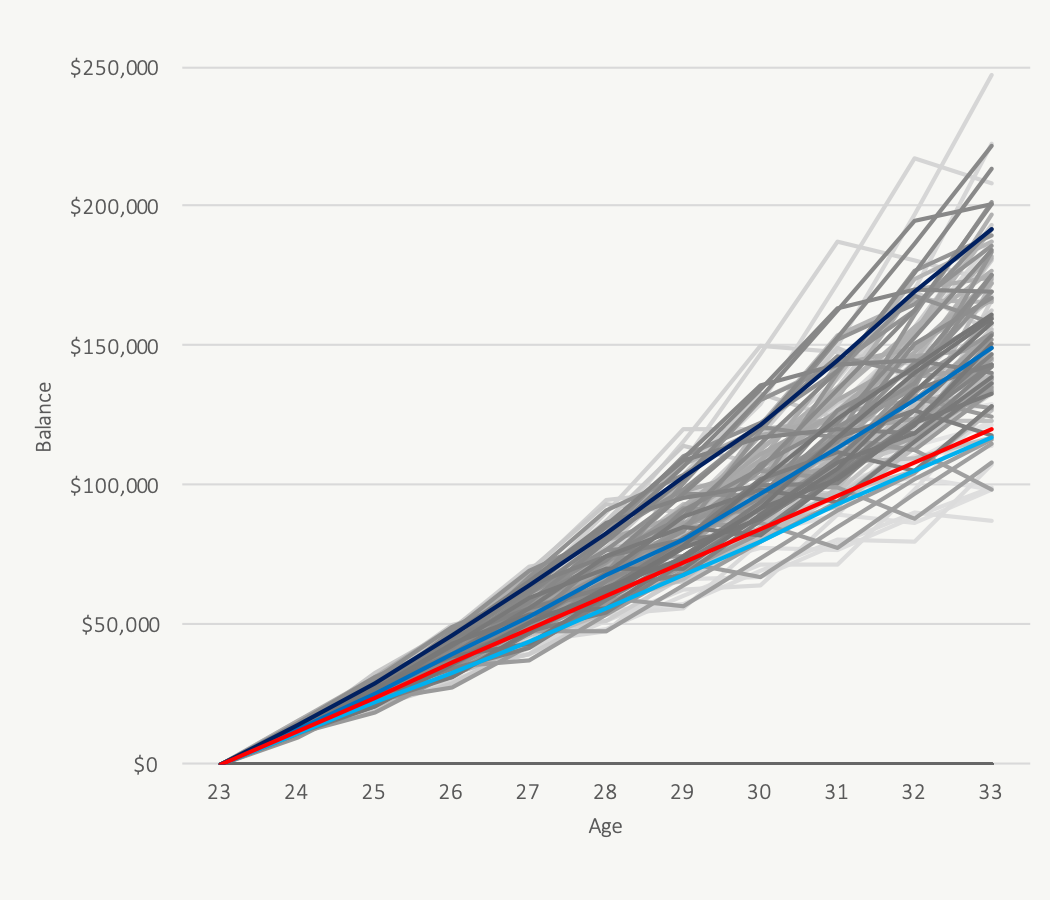

Saving And Investing Hybrid Over x Years

Each line in this chart represents one historical period of stock, bond, and inflation rates. Notice how some lines end upward beneath our red "savings only" line? This is the hazard of investing a portion of the downpayment. Even over a 10-yr time horizon at that place is nonetheless a pretty expert adventure that we'll finish up with less than we would have if nosotros had simply saved in a loftier-interest savings account. This becomes worse when you consider than in these cases we would as well incur CMHC mortgage insurance fees.

About 10% of historical periods end up beneath the "savings but" line, which a pretty good take a chance of ending up with less than if you had just played it safe, but there are quite a few periods that end upwardly higher. So is the saving/investing hybrid a good strategy? Maybe for some, probably non for others, and definitely not when the time period is shorter.

Best Way To Relieve Coin For A House?

What is the best mode to salvage coin for a firm? That depends on your time frame and your personal take a chance tolerance. If y'all take a longer time frame yous may consider investing some of your annual savings, especially if y'all don't have a clear goal for when and where you'll buy your future habitation. But y'all should always keep at to the lowest degree 5% of your down payment in a salvage investment vehicle like a high-interest savings account or a GIC.

For anyone with a curt fourth dimension frame (less than 5 years) the all-time mode to save money for a house is with a high-interest savings account or GIC. A safe investment vehicle similar these ii options volition ensure that y'all accept the money ready to get when yous need to make the final purchase. Anything else would be likewise risky.

Disclaimer: Historical results are a skillful examination but they don't fully capture the range of investment returns we may expect in the future. As they say "past performance does not guarantee futurity results" so be ready to end up with less if you're going to have on extra risk.

dominguezwitchany82.blogspot.com

Source: https://www.planeasy.ca/best-way-to-save-money-for-a-house/

0 Response to "Best Way to Invest and Save for a House"

Postar um comentário